13 September 2023

Since December 2021, the Bank of England (BoE) has raised the base interest rate 14 consecutive times in order to combat rising inflation.

This comes after the institution lowered the rate to just 0.1%, a historic low, in the face of the Covid-19 pandemic. In August, the BoE’s Monetary Policy Committee (MPC) raised the rate to 5.25%, and voted to maintain it at this level in September too.

When the BoE raises or drops rates, lenders tend to follow suit – and that is exactly what has been happening since December 2021.

As a result, the cost of mortgage agreements and other forms of borrowing have increased rapidly. While this is unwelcome news for consumers, there’s another side to this coin: interest rates are rising everywhere, meaning the interest earned on cash savings has shot up too.

Indeed, Moneyfacts reports that as of 21 September 2023, savers can gain a 5.1% interest rate on an easy access savings account.

As interest rates have risen, cash has become a more popular asset class again, after consumers experienced more than a decade of meagre returns. Which? reports that a record of £12 billion was deposited into Cash ISAs in April 2023 alone.

Plus, in the same time period, the stock market has been noticeably volatile. So, you could be wondering: “If interest on cash is high, and markets are unstable, why should I bother investing?”

While the picture seems clear now, things are more complicated than they appear on the surface.

Keep reading to find out three key reasons to consider staying invested despite higher cash returns.

1. A “no risk” cash strategy contains hidden long-term pitfalls

One of the key reasons many people choose cash over equities is that there’s little to no risk of losing money when it sits in cash. Investing, on the other hand, mostly carries some risk of capital losses.

Couple this with the possibility of a 5% return on your cash, and the opportunity to store your money away safely may be looking increasingly appealing.

However, cash can lull you into a false sense of security. Just like investment returns, interest rates fluctuate, and it’s unlikely that a 5% rate on your easy access or Cash ISA accounts will last forever.

Indeed, Moneyfacts reports that as of 7 September 2023, savers can gain a 5.1% interest rate on an easy access savings account.

While the BoE has not eased its interest rate hikes just yet, this could happen soon if inflation continues to inch closer to its 2% target. Furthermore, interest rates could then fall once inflation is under control.

So, while cash could seem like a low-risk, high-reward strategy at the moment, it’s important to take a long-term view. If interest rates drop, so too could the returns on your cash savings, leaving little room for growth in the decades to come.

2. High interest returns could push you above the Personal Savings Allowance

Whether you hold wealth in equities or cash, there’s always the possibility that you could pay tax on your returns.

Nevertheless, one often-overlooked aspect of having much of your wealth in cash is that when interest rates increase, the chance of you exceeding the Personal Savings Allowance (PSA) rises.

The PSA marks how much interest you can receive on your cash savings without the amount being added to your Income Tax bill for that year.

As of the 2023/24 tax year, the PSA is as follows:

- If you’re a basic-rate taxpayer, you can earn £1,000 a year in interest before paying Income Tax.

- Higher-rate taxpayers benefit from a PSA of £500.

- If you’re an additional-rate taxpayer, you do not have a PSA.

So, it’s important to remember that after a certain point, your non-ISA cash savings are not strictly “tax-free”. If you are a higher-rate taxpayer with a £500 PSA, you would only have to hold £10,000 in an account yielding 5% interest to reach your maximum limit – you’d then potentially pay Income Tax on any interest above that.

Cash ISAs are free from Income Tax, Capital Gains Tax (CGT) and the PSA, but it is applied to most other cash accounts. You can find in-depth insights into the PSA on our news page.

3. Historically, investing has beaten cash in the race to keep up with inflation

One of the most important reasons why staying invested could benefit you, even in a time of high cash returns, is that cash is highly unlikely to outpace inflation over time.

There is much evidence to suggest that keeping most or all of your wealth in cash may deplete its real-terms value over time – regardless of how interest rates fluctuate temporarily.

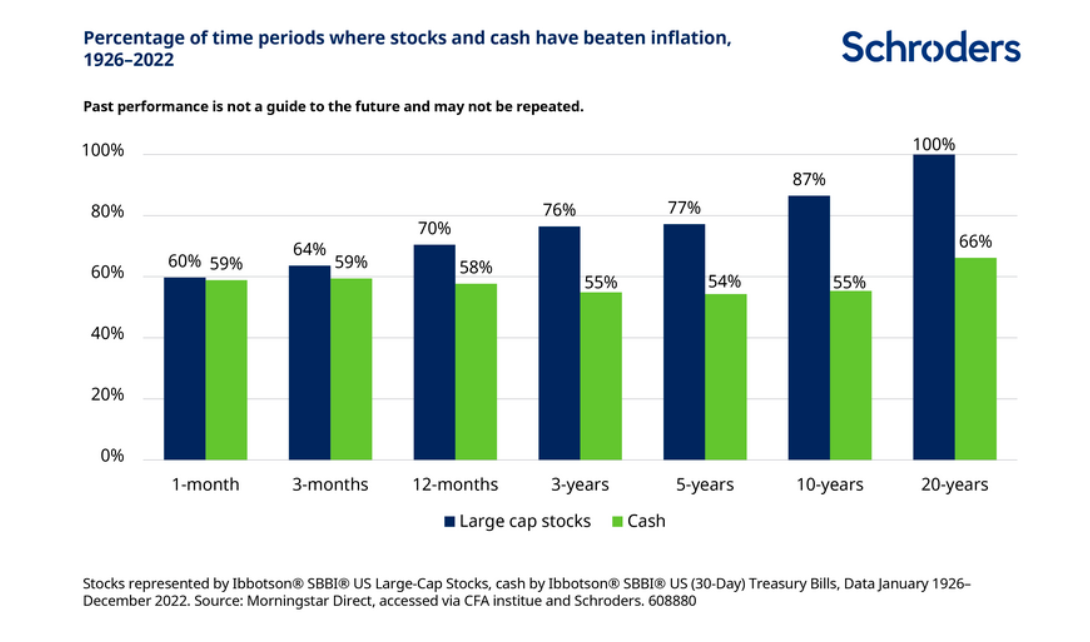

As you can see from the below graph, large cap stocks have routinely beaten inflation more often than cash over various time periods between 1926 and 2022.

Source: Schroders

Crucially, the historical long-term benefits of investing versus cash are evident here: large cap stocks outpaced inflation in 100% of circumstances when measured over 20 years. Conversely, cash only did the same 66% of the time.

Remember that the value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

However, staying invested could mean your wealth remains buoyant even as interest rates rise and fall over time.

This is not to say that cash savings shouldn’t form part of your financial plan. Cash can be helpful for emergencies, paying for one-off expenses, and day-to-day spending.

We can help you balance your cash with an investment portfolio that may help to grow your wealth over a period of years. With this in mind, you may be able to more easily plan for retirement, later-life care, or leaving a legacy to the next generation.

Get in touch

For expert advice on balancing your investments with cash, email info@depledgeswm.com or call 0161 8080200.

Please note

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

Levels, bases of and reliefs from taxation may be subject to change and their value depends on the individual circumstances of the investor.

The Financial Conduct Authority does not regulate tax advice.

All contents are based on our understanding of HMRC legislation, which is subject to change.

Comments on 3 important reasons to consider staying invested, even when cash offers high returns

There are 0 comments on 3 important reasons to consider staying invested, even when cash offers high returns