12 June 2023

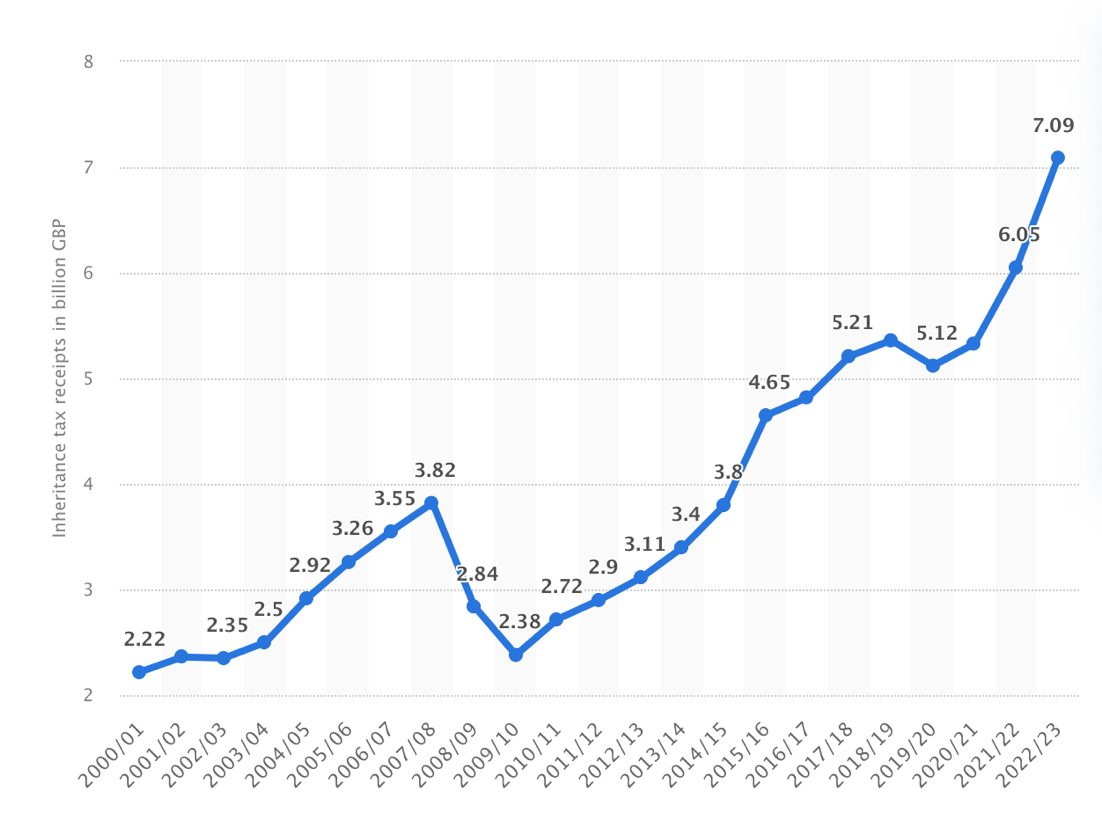

The UK government raised a record £7.1 billion in Inheritance Tax (IHT) during the 2022/23 financial year. Compared to the previous tax year, HMRC’s figures show that IHT takings have grown by £1 billion.

The chart below shows the steep trajectory in IHT tax receipts in the UK from 2000/01 to 2022/23.

Source: Statista

This doesn’t make for a pretty picture, and you may be concerned that an IHT charge on your estate may mean that less of your wealth is passed on to your family and loved ones.

The good news is that with some careful consideration and tax-efficient estate planning, it’s possible to reduce a potential IHT liability.

IHT thresholds have been frozen until 2028

IHT rules allow you to pass on an estate up to the value of £325,000 free of IHT. However, anything above this nil-rate band will typically incur a 40% tax charge.

Should you leave your primary residence to a child or grandchildren (including adopted, foster, or stepchildren), you receive an additional allowance worth £175,000. This is called the “residence nil-rate band”.

The government has frozen each of these allowances until at least 2028. As a result, many more estates can expect to face an unwelcome tax charge in the coming years.

2 ways you could mitigate a potential IHT bill

1. Consider “giving while living”

Making financial gifts while you’re still alive can be a useful way to avoid leaving a substantial IHT bill. One happy advantage of this is that you’ll be able to observe the benefits of your generosity and relax knowing that your loved ones are safe and secure in life.

There are several tax-efficient ways to gift money and help you avoid or reduce an IHT bill.

Here are some of the ways you could gift your money without incurring IHT:

- Annual gifts of up to £3,000 (2023/24 tax year). This uses your annual exemption – a tax-efficient benefit that you can use each tax year. This exemption can be carried forward for one year.

- Wedding gifts (or civil partnership gifts) that can be given to your friends and family at rates of up to £5,000 for your children, £2,500 for your grandchildren or great-grandchildren, or £1,000 to any other individual.

- Small gifts of up to £250 to any individual in a single tax year (not available where the gift recipient has received any larger gift from you in that tax year).

You can also make gifts from income. This may be something you choose to do if you want to help with someone’s living costs, for example.

You’re allowed to gift as much as you like, as long as:

- Your gifts are from income, not capital

- The gifts are regular

- You can afford to make the payments without affecting your own standard of living.

You could use this exemption to provide financial support your grown-up children during the cost of living crisis, help an elderly relative, or to pay into a savings account for a child under the age of 18.

To help show HMRC that you have met all the rules and requirements of gifting from income, it’s important to keep good records of the money you are giving.

2. Talk to your financial planner about trusts

Trusts can help you to control what happens to your assets after you pass away. If, for example, you want to set aside money for your children or grandchildren for the future, a trust may be an option to consider.

When you put property, cash, or other assets into a trust, provided you meet certain criteria, they no longer belong to you. As a result, when you die their value won’t normally be included for IHT calculations.

Beware though: trusts aren’t automatically exempt from IHT. If the amount you put in trust is above the nil-rate band, you may be liable to pay tax at 20% on the excess. However, there are some exceptions to this.

Since using a trust generally means giving up control of an asset, you need to be sure it’s an appropriate option for you.

It’s also vital to ensure the trust is set up in the correct way and in line with your wishes, which is why we recommend speaking to an experienced financial planner.

Get in touch

If you’d like help creating an estate plan designed to navigate these sometime complicated IHT rules, please get in touch.

Email info@depledgeswm.com or call 0161 8080200.

Please note

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

Levels, bases of and reliefs from taxation may be subject to change and their value depends on the individual circumstances of the investor.

The Financial Conduct Authority does not regulate tax advice.

Comments on 2 important estate planning tips for high earners facing a large Inheritance Tax bill

There are 0 comments on 2 important estate planning tips for high earners facing a large Inheritance Tax bill